Which blockbuster cancer biologics lose exclusivity, when biosimilars enter, and what the next wave – led by Keytruda's $25bn 2028 cliff – means for developers, payers and investors. Built on FDA Purple and Orange Book data.

$9.6bn

Market, 2025

Global oncology biosimilars, on a path to $17.5bn by 2030

76–90%

Wave 1 share

Biosimilar volume already captured on the first antibodies

$25bn+

Keytruda cliff

Revenue exposed at the 2028 U.S. loss of exclusivity

50–70%

Price discount

Typical ASP erosion at biosimilar steady state

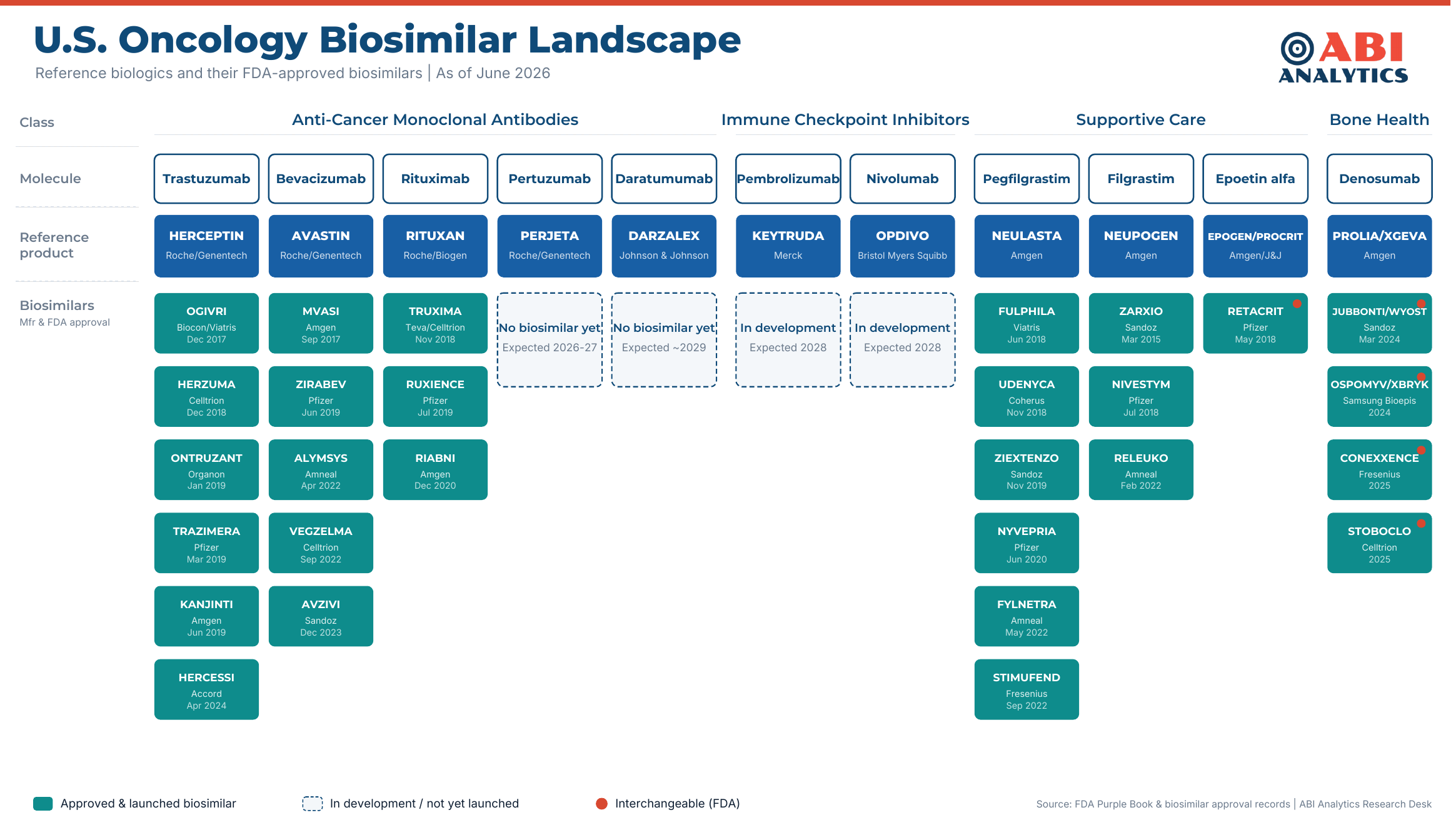

Fourteen pages of analysis tracing the two-wave structure of oncology biosimilar competition, from the now-commoditised first wave to the immuno-oncology cliffs that define the rest of the decade.

A few of the visuals you'll find in the full PDF. Scroll across to preview the landscape infographic, the cliff timeline and the molecule-level analysis.

← Scroll to explore | download the full report below for the complete analysis

Tell us where to send it. We'll unlock the download immediately and email you a copy, plus a note when we publish new therapeutic-area editions.

Your download should begin automatically. If it doesn't, use the button below.

Download PDF againWe produce bespoke biosimilar and patent-cliff landscapes for any therapeutic area, on your target molecules, timelines and competitive set.

Immunology

Adalimumab, ustekinumab, the TNF and IL franchises

Request →Diabetes and Metabolic

Insulins, GLP-1s and the next biosimilar wave

Request →Ophthalmology

Aflibercept, ranibizumab and retinal biologics

Request →Neurology

MS and migraine biologics facing exclusivity loss

Request →Respiratory

Asthma and COPD biologics and inhaled portfolios

Request →Custom scope

Your molecule list, markets and timelines

Request →